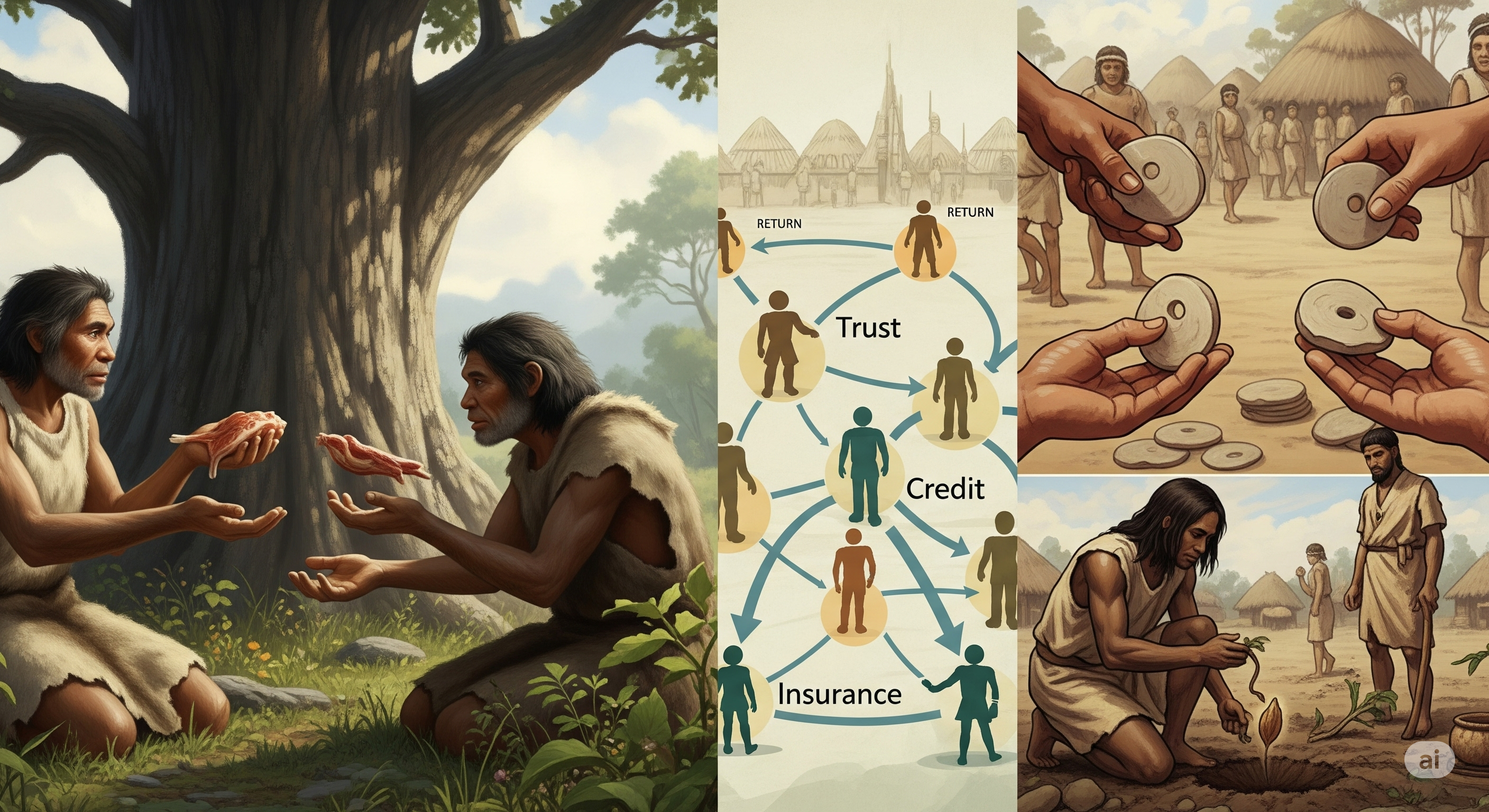

TL;DR for operators Most financial systems are designed as if finance begins with institutions: contracts, lenders, insurers, markets, prices, and enforcement. Paper 2506.00099 asks a cleaner question: what if the core behaviours behind finance emerge before those institutions, from repeated reciprocal interaction?1

The paper’s central move is to treat trade as the simplest case of reciprocity, then derive credit, insurance, token exchange, and investment as structural extensions of the same mechanism. Add delay, and reciprocity starts to look like credit. Add asymmetric risk, and it starts to look like insurance. Add portable mediation, and it starts to look like token exchange. Add expected future reward, and it starts to look like investment. Finance, in this view, is not born fully dressed in a suit carrying a term sheet. It begins as remembered obligation.

...