TL;DR for operators

Most financial systems are designed as if finance begins with institutions: contracts, lenders, insurers, markets, prices, and enforcement. Paper 2506.00099 asks a cleaner question: what if the core behaviours behind finance emerge before those institutions, from repeated reciprocal interaction?1

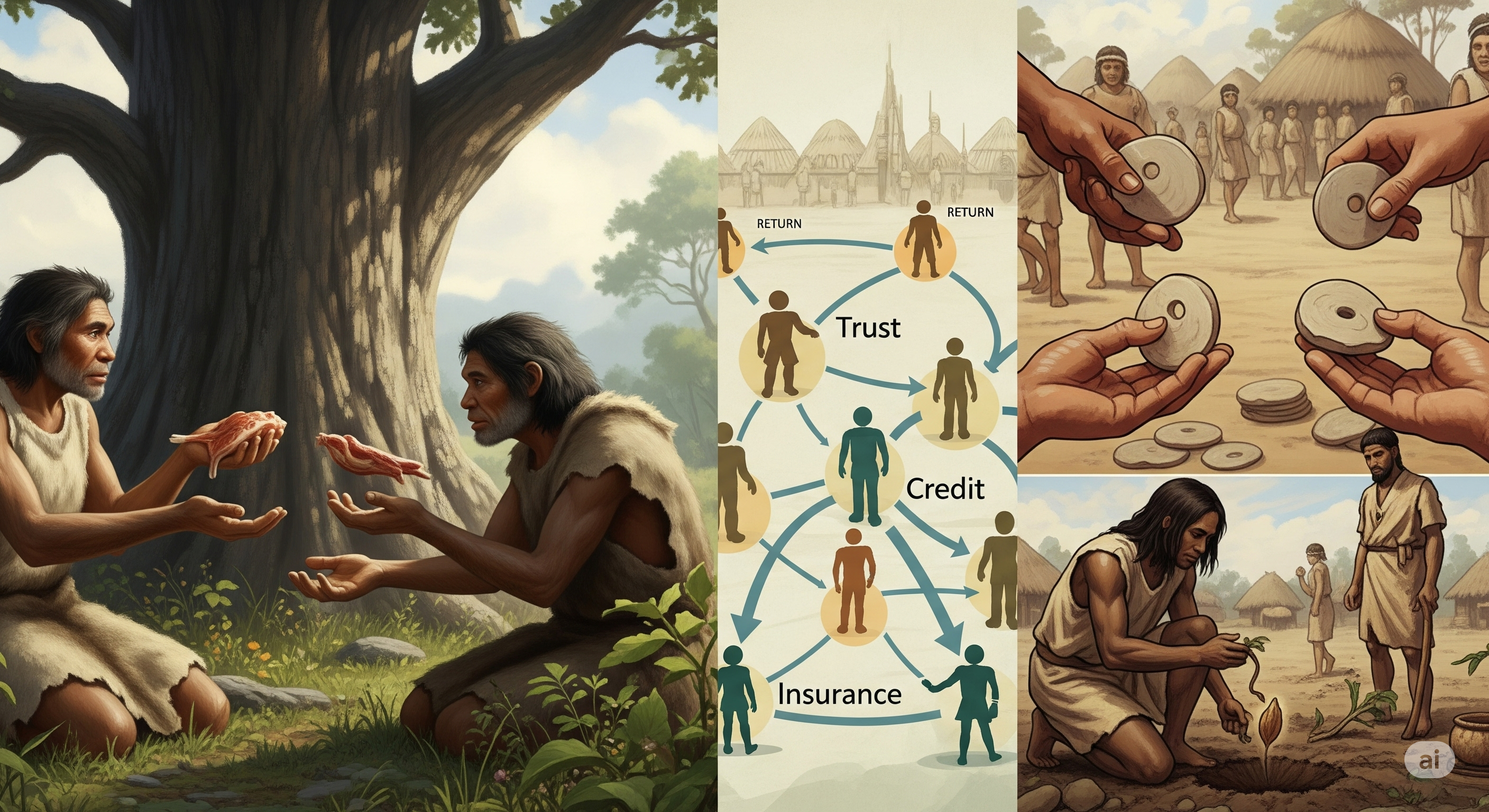

The paper’s central move is to treat trade as the simplest case of reciprocity, then derive credit, insurance, token exchange, and investment as structural extensions of the same mechanism. Add delay, and reciprocity starts to look like credit. Add asymmetric risk, and it starts to look like insurance. Add portable mediation, and it starts to look like token exchange. Add expected future reward, and it starts to look like investment. Finance, in this view, is not born fully dressed in a suit carrying a term sheet. It begins as remembered obligation.

For operators building AI-agent markets, trust layers, decentralized platforms, or simulation environments, the useful takeaway is not “biology explains finance.” That would be too neat, and therefore suspicious. The useful takeaway is that finance-like behaviour may be modelled from a minimal substrate: partner recognition, memory of past interaction, reciprocity scoring, and behavioural updating. Instead of hardcoding an agent as a lender, insurer, trader, or investor, a simulation can ask whether those roles emerge from local interactions.

The paper does not present a calibrated market model, a new empirical dataset, or a working financial simulator. Its contribution is architectural and conceptual: it gives researchers a way to specify what to look for when finance-like macrostates emerge in multi-agent systems. The business implication is design discipline. If a platform wants durable cooperation, delayed repayment, risk sharing, or indirect exchange, it should not only design incentives. It should design memory, reputation, obligation, and reversibility.

The boundary is equally important. Reciprocity may be necessary for many financial behaviours, but it is not sufficient for modern finance at scale. Law, accounting, symbolic abstraction, liquidity, enforcement, cultural norms, and institutional credibility still matter. Yes, unfortunately, finance remains complicated. The paper’s value is that it identifies the behavioural root system under the concrete.

A favour is a primitive financial instrument

Start with a familiar situation. One person covers lunch because the other forgot their wallet. No contract is signed. No interest rate is negotiated. No collateral is posted. Yet something financially recognisable has happened: a resource moved now, and an expectation moved into the future.

That expectation is not yet credit in the institutional sense. It has no repayment schedule, default clause, or regulator pretending the spreadsheet captures reality. But it has the behavioural shape of credit: delayed return, remembered imbalance, and conditional future treatment.

This is the paper’s opening wedge. It argues that finance should not be reconstructed from markets downward, but from reciprocal behaviour upward. Classical financial theory often begins after the machinery already exists: assets, markets, clearing, contracts, rational agents, equilibrium. Behavioural finance then modifies the agent by adding biases, bounded rationality, loss aversion, mental accounting, and other human inconveniences. Both traditions are useful, but both often assume the stage on which finance already operates.

The paper asks what comes before the stage.

Its answer is reciprocity: the repeated, partner-contingent exchange of help, resources, or support, guided by memory and expectation. Reciprocity is attractive as a substrate because it is cognitively modest, socially observable, and empirically grounded across primate behaviour and early human economic life. The paper draws on work in primatology, anthropology, behavioural economics, and agent-based modelling to argue that financial behaviours can be reconstructed as transformations of reciprocal interaction rather than as separate institutional inventions.

This does not mean modern finance is “just” reciprocity. A derivatives desk is not a bonobo grooming circle with Bloomberg terminals. The claim is narrower and more useful: before finance becomes institutional infrastructure, its functional shapes may emerge from recurring social imbalances that agents learn to manage.

The paper’s mechanism: finance as reciprocity under constraints

The mechanism-first reading is the right one because the paper is not primarily reporting a benchmark, an experiment, or a numerical result. It is building a generative map.

The basic form is trade. Trade is simultaneous, symmetric, and partner-contingent. I give, you give, and both sides can observe the exchange. In this framing, trade is not finance’s ancestor in a separate category. It is reciprocity in its most compressed form.

From there, finance emerges when the same reciprocal structure is stretched or modified by four constraints.

| Reciprocity condition | Financial behaviour | What changes | Operational interpretation |

|---|---|---|---|

| Simultaneous exchange | Trade | Give and return occur together | Baseline reciprocal exchange |

| Time delay | Credit | Return is deferred | Memory turns imbalance into obligation |

| Asymmetric risk | Insurance | Help depends on need under uncertainty | Role reversibility turns support into pooling |

| Scalable mediation | Token exchange | Obligation is represented indirectly | Tokens replace direct partner memory |

| Expected future reward | Investment | Contribution targets uncertain future gain | Projection turns sacrifice into expected return |

This table is the paper’s thesis in operator language. Finance is not treated as a list of institutions. It is treated as a family of interaction patterns.

The important shift is that the financial category is defined by behaviour, not by labels. An agent does not need to be called a “borrower” to participate in credit-like dynamics. It needs to receive resources now, generate a remembered imbalance, and later reciprocate. A group does not need a formal insurer to show insurance-like behaviour. It needs to redistribute support under stochastic harm in a way that stabilises mutual survival. Tokens do not need a central bank to function as token exchange. They need to mediate indirect reciprocity across agents who do not share direct histories.

That distinction matters for artificial agent economies. If every role is hardcoded, the simulation demonstrates the designer’s assumptions. If roles emerge from memory, scoring, and updating, the simulation may reveal conditions under which financial structures actually stabilise.

Credit begins when imbalance survives the moment

The paper’s first transformation is reciprocity plus time delay.

In direct trade, the balance closes immediately. In credit-like behaviour, the balance remains open. One agent gives now and relies on memory, recognition, and future interaction to make return plausible later. The paper describes this as a form of social debt: not formal debt, but an imbalance that alters future behaviour.

The evidence here is not a new credit experiment. It is a behavioural grounding. The paper points to primate observations where grooming, food sharing, and coalitionary support may occur without immediate return, as well as human evidence around indebtedness, guilt aversion, and repeated trust games. The function of this evidence is to support plausibility: delayed reciprocity can exist without formal enforcement.

That is a modest claim, but a useful one. In many digital systems, designers try to manufacture credit through rules first: credit scores, collateral, legal identity, escrow, penalties. Those tools matter. But the paper implies that the deeper primitive is remembered imbalance. If the system cannot remember who absorbed cost, who returned value, and how quickly imbalance closed, then it has weak behavioural soil for credit.

For AI-agent markets, the design lesson is straightforward: credit-like behaviour requires more than a lending module. It requires persistent partner-specific memory and a mechanism for updating future willingness to cooperate.

A minimal credit-like signal might look like this:

The exact formula is not in the paper, and should not be smuggled in as if it were. The point is architectural. Agents need some way of representing imbalance over time. Without that, “credit” is just a scripted transfer followed by a scripted repayment. Very tidy. Also very uninteresting.

Insurance emerges when reciprocity stops being exact

Credit still preserves a sense of bilateral balance: I helped you, so you help me later. Insurance is stranger. It requires agents to support others not because exact repayment is due, but because misfortune is uneven and roles may reverse.

The paper frames insurance as reciprocity under asymmetric risk and uncertainty. When harm arrives randomly, the relevant question changes from “Who owes whom?” to “Who needs support now, and can the group survive if support circulates when needed?”

This is where the paper’s use of field and modelling evidence matters. It references food sharing among hunter-gatherers and agent-based simulations of Maasai livestock exchange under the osotua norm. The purpose of this evidence is not to claim that modern insurance descends linearly from one cultural practice. It is to show that risk-buffering reciprocity can stabilise under decentralized conditions when agents face uneven shocks and repeated dependence.

That distinction is crucial. Insurance-like behaviour is not merely generosity with better branding. It requires a structure in which helping the currently unlucky is sensible because the unlucky position is reversible. If the same agents are always donors and the same agents are always recipients, the system becomes hierarchy, taxation, charity, exploitation, or collapse, depending on taste and spreadsheet formatting.

For business design, the implication is that risk-pooling systems need to encode need, uncertainty, and role reversibility. Mutual aid networks, decentralized insurance protocols, and agent-based resource-sharing systems fail when they treat every transfer as a simple bilateral debt. Under genuine uncertainty, exact accounting can become too rigid. Insurance requires tolerance for imbalance, as long as the imbalance is justified by stochastic need and expected future role reversal.

This is one of the paper’s most practical insights. Some cooperative systems die not because people dislike cooperation, but because the accounting grammar is wrong. They use credit logic where insurance logic is needed.

Tokens scale reciprocity by replacing personal memory

Direct reciprocity has a scaling problem: memory does not travel well.

In small groups, agents can remember who helped whom. In larger networks, dyadic memory becomes expensive, incomplete, or impossible. Token exchange solves this by externalising part of the memory burden. A token becomes a portable representation of prior contribution, claim, or value. It allows cooperation to move through indirect chains rather than only through direct partner history.

The paper calls this reciprocity plus scalable mediation. This is the bridge from “I helped you” to “I hold something that others recognise as evidence of value.” Once that happens, exchange can expand beyond personal familiarity.

The paper is careful here. It notes that token-based mediation has received less direct developmental and comparative research than some other behaviours, partly because it is difficult to isolate experimentally. It points to children inventing placeholder tokens in cooperative play and non-human primates using arbitrary tokens in laboratory exchange as suggestive evidence that token mediation draws on general cognitive mechanisms. This is plausibility evidence, not a complete theory of money.

The business relevance is obvious but often mishandled. Crypto protocols, loyalty systems, reputation markets, marketplace credits, and internal platform currencies all use tokens to mediate exchange. But the paper suggests that the token is only doing real economic work if it preserves or transfers reciprocal meaning. Otherwise, it is decoration with a ticker symbol.

A token can mediate reciprocity only if participants believe it reliably answers at least three questions:

| Question | Why it matters |

|---|---|

| What past contribution or claim does this token represent? | Without provenance, the token is arbitrary. |

| Who will recognise it in future exchange? | Without acceptance, it cannot scale reciprocity. |

| Can it move across relationships without destroying trust? | Without transferability or credible constraint, mediation fails. |

This is why token design is not just issuance. It is memory architecture. The token must compress interaction history into a form other agents can accept without knowing the original partner. That compression is powerful. It is also where fraud, speculation, and empty tokenomics stroll in wearing sunglasses.

Investment is reciprocity aimed at an uncertain future

The final transformation is reciprocity plus expected future reward.

Investment differs from simple delayed reciprocity because the future return is uncertain and often depends on other agents’ future actions. I give resources now not merely because someone owes me later, but because I expect the contribution to generate a larger future return. That requires delay tolerance, projection, and social inference.

The paper grounds this mechanism in evidence around delayed gratification, primate intertemporal choice, trust games, and delayed reciprocity. Again, this is not a new investment experiment. The purpose is to show that the cognitive components of investment behaviour—waiting, projecting, and accepting uncertainty—exist before formal investment institutions.

For operators, the key point is that investment is not just delayed payoff. A vending machine with a timer is not a venture ecosystem. Investment-like behaviour is socially contingent: returns depend on whether others coordinate, reciprocate, build, honour claims, or sustain the system long enough for future value to appear.

This matters for AI-agent environments where agents allocate compute, capital, attention, inventory, or data to future opportunities. A system that wants investment-like behaviour must support:

- memory of prior contributions;

- estimation of future returns;

- uncertainty over outcomes;

- dependence on others’ future behaviour;

- adjustment after success, failure, or non-reciprocation.

If those elements are absent, “investment” becomes a one-step optimisation problem. Useful, perhaps, but not the phenomenon the paper is trying to reconstruct.

The simulateable substrate is deliberately minimal

The paper’s second contribution is the move from conceptual anthropology to simulation architecture. It proposes a lightweight substrate for modelling finance-like emergence in multi-agent systems.

The substrate contains three main capacities:

| Agent capacity | Function in the framework | Finance-like behaviours it supports |

|---|---|---|

| Partner-specific memory | Records past cooperative and non-cooperative interactions | Credit, trust, delayed repayment |

| Reciprocal evaluation heuristics | Scores partners based on interaction history | Partner selection, cooperation, withdrawal |

| Behavioural updating | Changes future strategy based on reciprocity scores | Stable networks, exclusion of exploiters, emergent roles |

This is intentionally not a full economic model. There are no complete markets, no legal enforcement systems, no pricing theory, no balance sheets, no endogenous accounting standards, and no comforting illusion that three variables explain civilisation.

The point is to define a minimal behavioural layer on which more complex systems can be built. In particular, the paper argues that LLM-based agents could implement these mechanisms through structured memory and interaction protocols rather than through reinforcement learning alone. Agents would not need predefined economic roles. They would choose whom to engage, when to cooperate, and when to withhold cooperation based on remembered outcomes and anticipated returns.

That design choice matters. Many agent-based economic simulations begin by assigning roles: buyer, seller, lender, borrower, insurer. The result may be informative, but it cannot answer the emergence question. If the role is pre-installed, the simulation has not shown how the role appears.

The paper instead asks for behavioural criteria. We should examine interaction logs and ask whether distinctive macrostates have formed.

| Macrostate | Behavioural criterion in simulation | What it would support | What it would not prove |

|---|---|---|---|

| Credit | Persistent asymmetric contribution followed by delayed return | Delayed reciprocity can stabilise | Real-world credit markets will emerge |

| Insurance | Need-based support under stochastic harm | Risk pooling can arise from reciprocity | Actuarial pricing or solvency is solved |

| Token exchange | Indirect cooperation through transferable placeholders | Mediation can scale beyond dyadic memory | Tokens will hold stable market value |

| Investment | Costly action aimed at uncertain future social return | Agents can sacrifice now for projected future gain | Capital allocation will be efficient |

This is the paper at its most useful for AI researchers and platform designers. It turns vague claims about “emergent economies” into observable behavioural tests. Not perfect tests. But better than watching agents swap imaginary apples and declaring a civilisation.

What the paper directly shows

The paper directly shows a conceptual reconstruction, not an empirical demonstration. That matters.

It shows that a family resemblance exists among trade, credit, insurance, token exchange, and investment when each is described as a transformation of reciprocity. It also shows that these transformations can be mapped to minimal agent capacities that are plausible in both human and artificial systems.

It does not show that reciprocity alone explains modern finance. It does not show that a particular simulation produces all four behaviours. It does not estimate magnitudes, compare model variants, run ablations, or validate against market data. There are no benchmark scores to worship. Everyone can exhale.

The evidence base is synthetic. The paper draws on prior empirical findings from primatology, anthropology, behavioural experiments, and agent-based modelling. These references support the plausibility of each behavioural ingredient: delayed return, need-based support, token mediation, and future-oriented cooperation. Their role is grounding, not proof of a complete causal chain.

That makes the paper more like a design grammar than a finished machine.

What Cognaptus infers for business use

The most useful business inference is that financial product design should distinguish institutional wrappers from behavioural primitives.

A lending product is not only an interest rate plus repayment schedule. It is a system for tracking imbalance, updating trust, and deciding what happens after repayment, delay, or default. An insurance product is not only premium collection and claims processing. It is a system for pooling asymmetric harm without making contributors feel like permanent victims of someone else’s bad luck. A token system is not only issuance and transfer. It is a system for making past contribution legible across unfamiliar relationships. An investment platform is not only capital allocation. It is a system for projecting future reciprocal value under uncertainty.

That interpretation points to practical design questions:

| Product or system | Reciprocity primitive to inspect | Design question |

|---|---|---|

| AI-agent marketplace | Partner-specific memory | Do agents remember reliable counterparties and adjust future cooperation? |

| Decentralized credit | Delayed imbalance | How is non-return represented before formal default? |

| Mutual insurance | Need-based support | Can the system separate genuine stochastic harm from persistent extraction? |

| Token platform | Mediated obligation | What real claim, access, or reciprocal recognition does the token encode? |

| Agent investment system | Future-oriented reciprocity | How do agents estimate social return when outcomes depend on others? |

The ROI relevance is not immediate revenue uplift. It is diagnostic clarity. The framework helps teams avoid a common design mistake: implementing financial labels without the underlying behavioural conditions. Calling something “credit” does not make it credit-like if no one tracks obligation. Calling something “community insurance” does not make it insurance-like if the system cannot handle asymmetric shocks. Calling something a “utility token” does not make it useful if it mediates no credible reciprocal claim.

This is where the paper has quiet bite. It tells fintech and AI-system designers to stop confusing interface categories with behavioural functions. A button labelled “lend” is not a lending market. A token with a logo is not an economy. A multi-agent simulation with prices is not necessarily finance. Cruel, but fair.

The misconception to avoid: this is not biological determinism

The paper includes an ethical statement rejecting evolutionary teleology, cultural essentialism, and biological determinism. That warning is necessary.

Because the paper uses primate behaviour and early human societies as evidence, a careless reader could flatten the argument into “finance is natural.” That is not the claim. The paper is not saying credit cards were hiding in chimpanzee grooming patterns, patiently waiting for interchange fees.

The better reading is that certain behavioural capacities make finance-like structures possible: memory, partner recognition, delayed return tracking, risk-sensitive support, symbolic mediation, and future projection. These capacities can be observed in simpler forms before formal institutions. Human societies then stabilise, abstract, and scale them through culture, law, symbols, accounting, and technology.

The distinction matters because “natural” arguments are usually lazy. They make existing arrangements look inevitable. This paper is more interesting than that. It does not naturalise modern finance; it decomposes finance into behavioural requirements.

That decomposition is useful precisely because it allows variation. Different societies, platforms, and agent systems can implement the primitives differently. Some may rely on reputation. Others on collateral. Others on tokens. Others on legal enforcement. The substrate may be reciprocal, but the architecture is not predetermined.

Where the framework stops

The paper’s limitation is not a footnote; it is part of the interpretation.

First, the framework is not predictive. It does not forecast credit growth, insurance adoption, token value, investment returns, or market stability. Operators should not treat it as a model for pricing, underwriting, or portfolio allocation.

Second, reciprocity is not the only mechanism behind finance. Signalling, imitation, hierarchy, coercion, regulation, cultural learning, liquidity preference, accounting conventions, and institutional trust can all shape financial systems. The paper acknowledges that it isolates reciprocity as a sufficient behavioural substrate for reconstructing core functions, not as the entire causal universe.

Third, the framework needs simulation and experimental follow-through. The proposed architecture is simulateable, but the paper does not yet report a full simulation demonstrating the spontaneous emergence of all four macrostates under controlled conditions. That is future work.

Fourth, scaling remains hard. Dyadic reciprocity can explain local cooperation. Modern finance requires abstraction across millions of participants, legal enforceability, adversarial robustness, and mechanisms for dealing with strangers who will never meet again. Tokens help with scale, but tokens also introduce manipulation, speculation, and governance problems. Humanity invented ledgers for a reason. Also auditors, unfortunately.

Finally, LLM-based agents add a separate boundary. Structured memory and interaction protocols may allow agents to simulate reciprocal reasoning, but LLM behaviour can be brittle, prompt-sensitive, and performative. An agent saying it trusts another agent is not the same as a stable trust dynamic. Logs, incentives, and repeated behavioural evidence still matter.

The operator’s framework: design for the behaviour, not the label

A practical way to use the paper is to treat each financial function as a behavioural test.

Before building or evaluating a finance-like system, ask which transformation of reciprocity it depends on.

| If the system claims to enable… | Look for this behavioural pattern | Failure mode if absent |

|---|---|---|

| Trade | Immediate reciprocal exchange | The market is just allocation without mutual recognition |

| Credit | Delayed return after asymmetric contribution | Lending becomes scripted transfer or unsecured leakage |

| Insurance | Need-based support under uncertain harm | Pooling becomes charity, subsidy, or extraction |

| Token exchange | Indirect reciprocity through recognised placeholders | The token becomes symbolic clutter |

| Investment | Costly present action for uncertain future social return | Capital allocation becomes short-term optimisation |

This is a useful diagnostic because many platforms adopt financial vocabulary early. The vocabulary arrives before the behaviour. The pitch deck says “ecosystem,” “incentives,” “trust layer,” and “capital formation.” The interaction logs say: three bots farm rewards, nobody reciprocates, and the token mediates nothing except exit liquidity. A timeless genre.

The paper gives a cleaner inspection method. Do not ask whether the system has financial nouns. Ask whether agents are forming financial verbs: giving, remembering, returning, buffering, mediating, projecting, withholding, and updating.

Conclusion: finance starts before finance

The strongest idea in the paper is that finance may begin before finance has a name.

Trade is reciprocal exchange compressed into the present. Credit stretches reciprocity across time. Insurance bends it around uncertainty. Token exchange externalises it into portable mediation. Investment points it toward uncertain future return. Each step adds abstraction, but the root remains interaction plus memory.

For business readers, the payoff is not philosophical decoration. It is design clarity. If we want AI agents, decentralized platforms, or fintech systems to support durable financial behaviour, we need to model the substrate beneath the institution. That means tracking relationships, obligations, risk exposure, indirect claims, and future-oriented expectations.

Institutions still matter. Contracts still matter. Regulation still matters. Accounting definitely matters, because someone must eventually ruin the poetry with reconciliation. But the paper’s useful provocation is that these are stabilisers of financial behaviour, not necessarily its origin.

Finance, before it becomes a market, is a pattern of remembered cooperation under constraint. That may be less glamorous than “the future of money.” It is also more likely to survive contact with reality.

Cognaptus: Automate the Present, Incubate the Future.

-

Egil Diau, “Finance as Extended Biology: Reciprocity as the Cognitive Substrate of Financial Behavior,” arXiv:2506.00099, 2025, https://arxiv.org/abs/2506.00099. ↩︎