Noisy by Nature: Rethinking Financial Time Series Generation with GBM-Inspired Diffusion

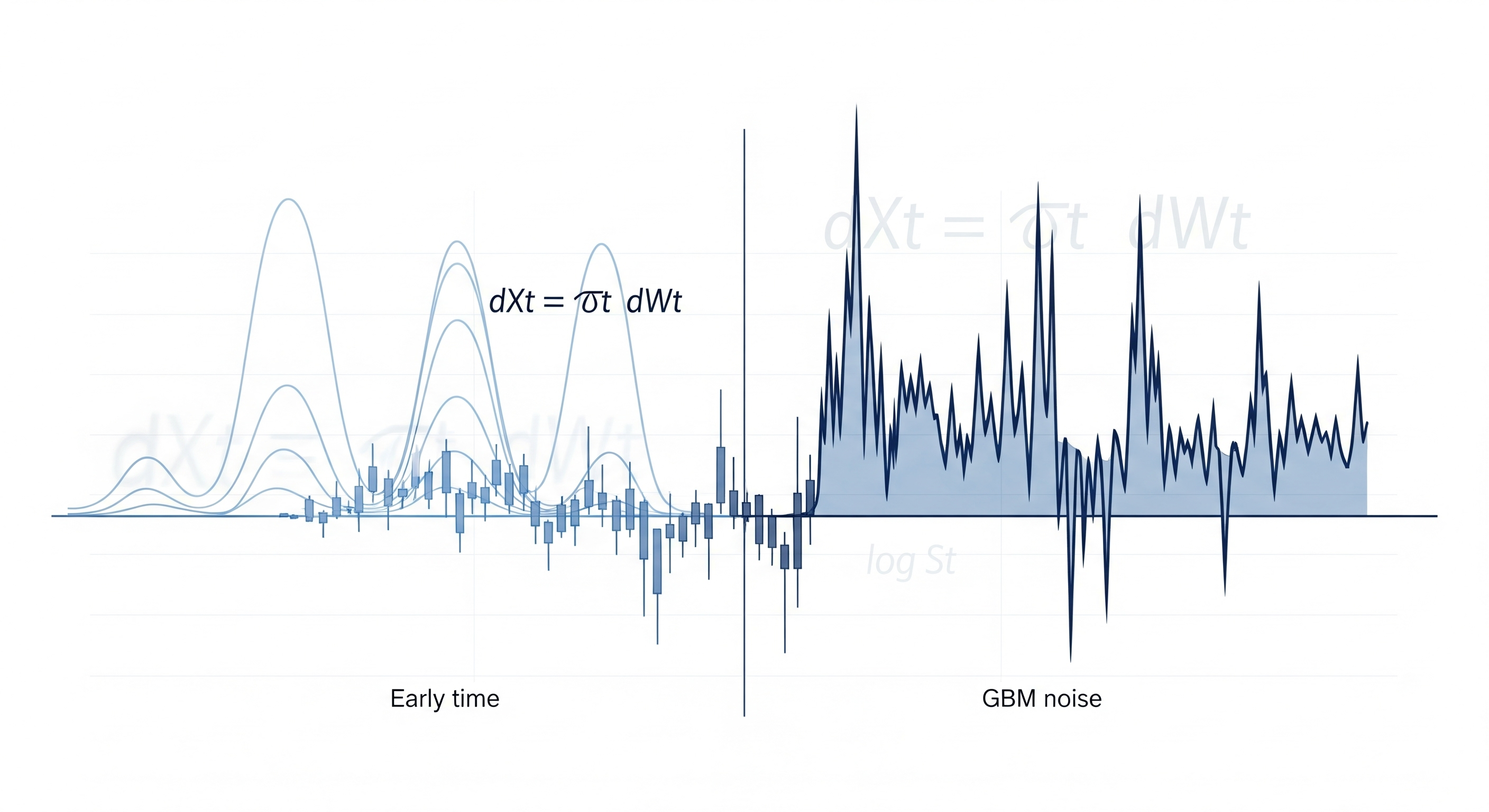

TL;DR for operators Financial time series generation has a surprisingly basic problem: many models corrupt market data as if prices were pixels. Add Gaussian noise, train a neural network to remove it, admire the architecture, and then wonder why the generated series behave like polite laboratory specimens rather than markets. Kim, Choi, and Kim’s paper proposes a more finance-native diffusion design: use geometric Brownian motion (GBM) as an inductive bias in the forward noising process.1 The point is not to revive Black–Scholes as a complete market simulator. The point is narrower and more useful: make the noising process respect the fact that asset prices move multiplicatively and volatility scales with price level. ...