Noisy by Nature: Rethinking Financial Time Series Generation with GBM-Inspired Diffusion

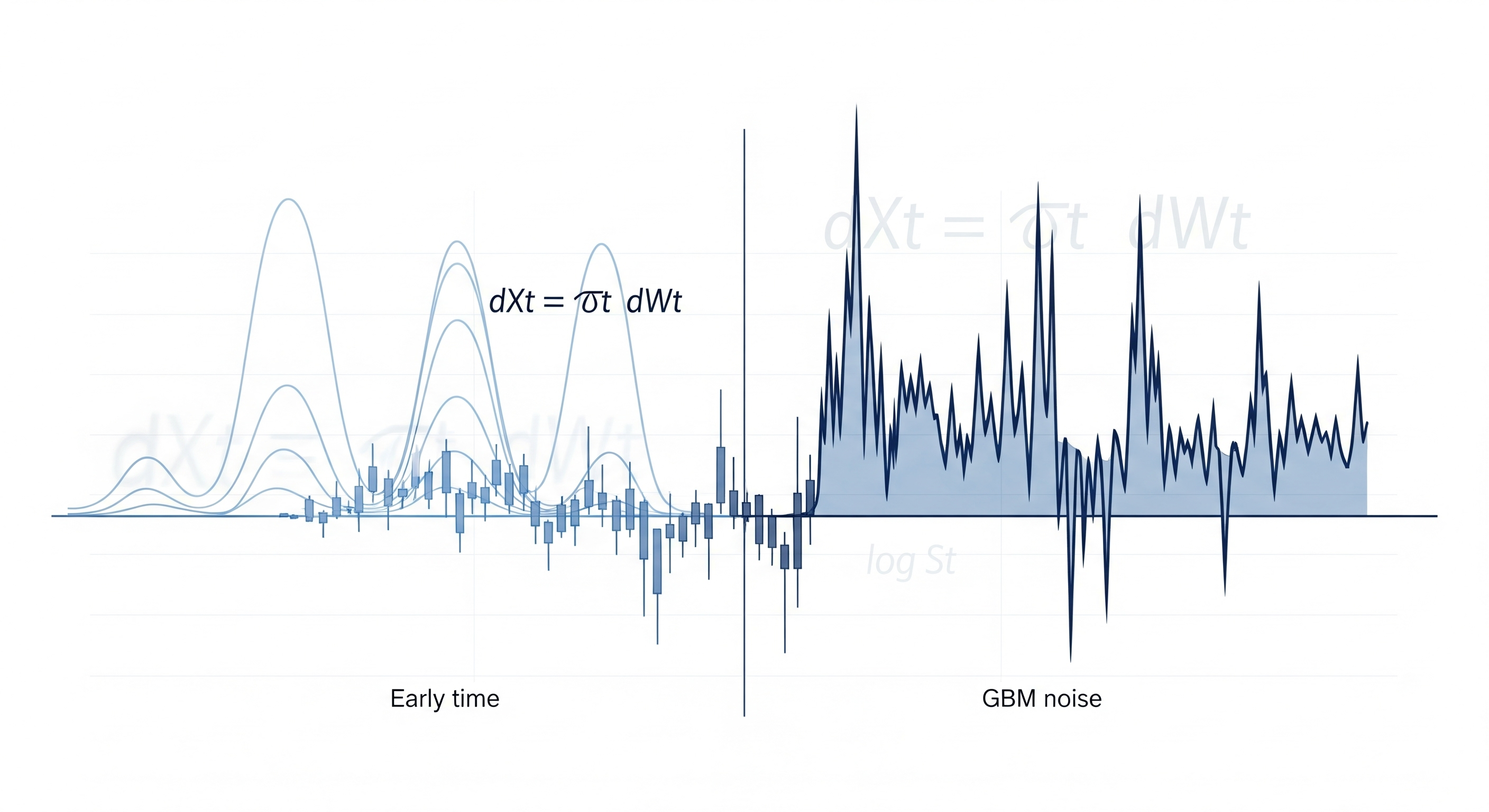

Most generative models for time series—particularly those borrowed from image generation—treat financial prices like any other numerical data: throw in Gaussian noise, then learn to clean it up. But markets aren’t like pixels. Financial time series have unique structures: they evolve multiplicatively, exhibit heteroskedasticity, and follow stochastic dynamics that traditional diffusion models ignore. In this week’s standout paper, “A diffusion-based generative model for financial time series via geometric Brownian motion,” Kim et al. propose a subtle yet profound twist: model the noise using financial theory, specifically geometric Brownian motion (GBM), rather than injecting it naively. ...