Boxed In, Cashed Out: Deep Gradient Flows for Fast American Option Pricing

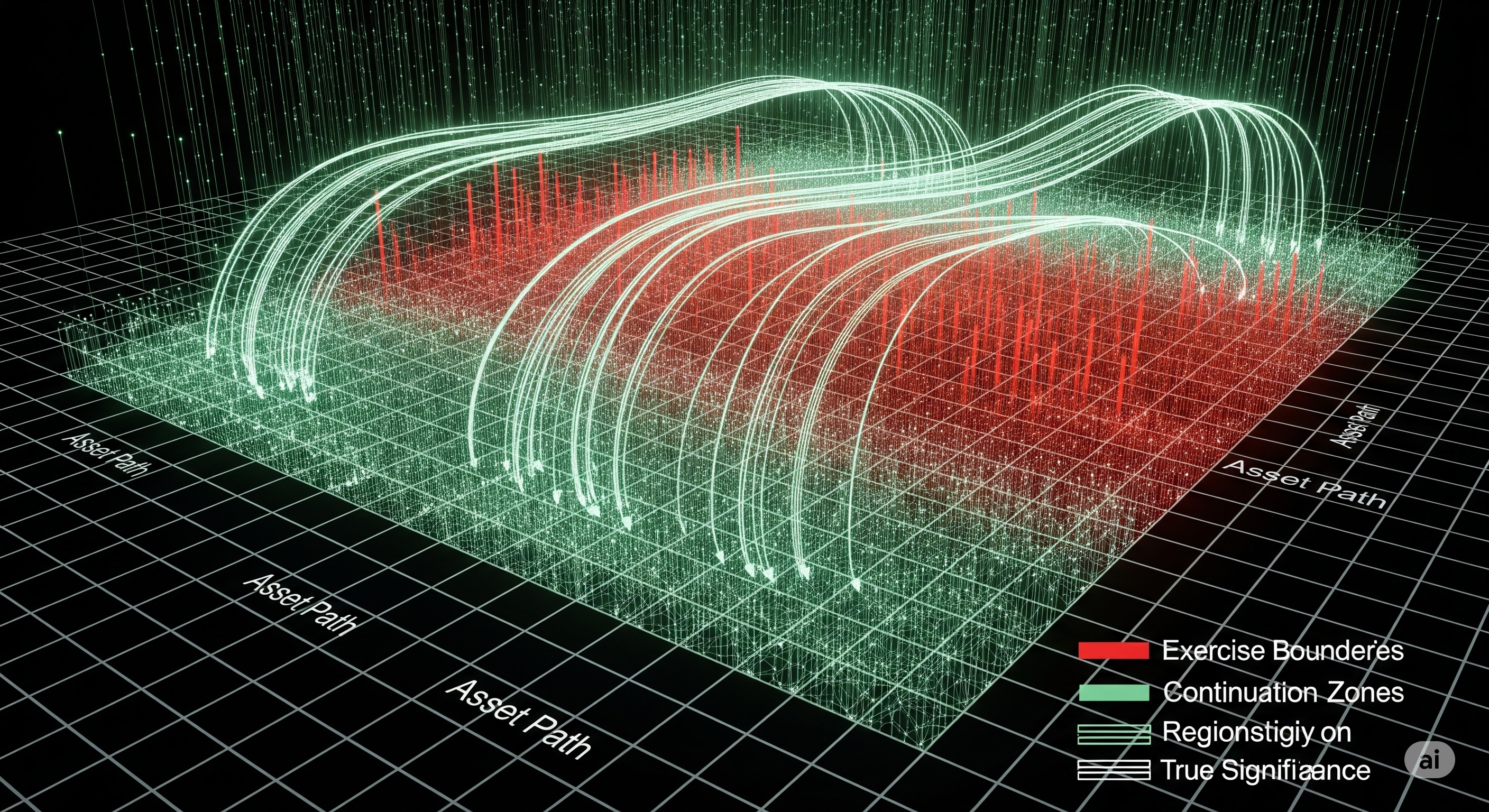

TL;DR for operators American options are awkward because the model must decide not only what the contract is worth, but also where exercise becomes optimal. That turns pricing into a free-boundary problem, which is exactly the kind of thing that makes high-dimensional PDE methods start sweating through their nice academic shirts. Jasper Rou’s paper extends Time Deep Gradient Flow (TDGF) to American basket put options under multidimensional Black-Scholes and Heston models.1 The useful trick is not “throw a neural network at finance”. We have tried that spell before; it produces PowerPoint before it produces risk control. The actual mechanism is more specific: TDGF trains a neural PDE solver through time steps, only applies the PDE loss in the continuation region, and builds the payoff floor into the network so the model cannot price below the intrinsic value. ...