Volume Shock Therapy: Why Markowitz Risk Might Be Lying to You

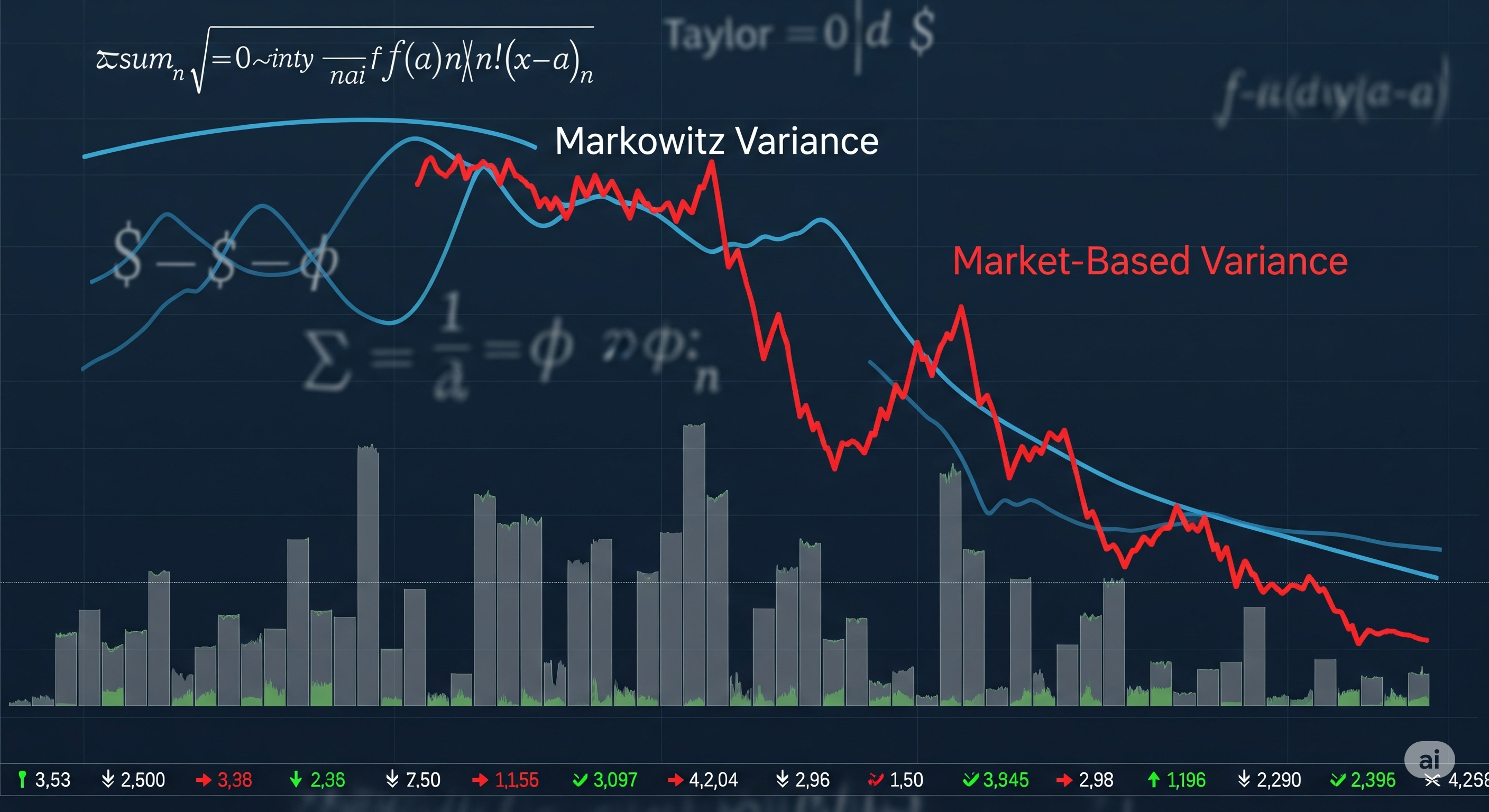

TL;DR for operators Markowitz variance is usually treated as the clean mathematical backbone of portfolio risk. Olkhov’s paper asks a narrower and more awkward question: what if that familiar covariance formula is only what remains after trade-volume randomness has been quietly set to zero?1 The paper’s answer is mechanism-first. It constructs a buy-and-hold portfolio as if it were a synthetic single traded security. To do that, it rescales the observed market trades of each constituent so their normalised volumes match the investor’s actual holdings, then aggregates those normalised trade values and volumes into portfolio-level trade series. Once the portfolio has its own synthetic trade values $Q(t_i)$, volumes $W(t_i)$, and implied prices $s(t_i)$, its variance can be computed in the same market-based way as the variance of any single security. ...